Federal Direct Loans

You may be eligible for Federal Direct Loans and can determine your eligibility by completing the Free Application for Federal Student Aid (FAFSA) and enrolling at least half-time.

Subsidized Loans

Subsidized loans are awarded based on financial need. No interest is charged before you begin repayment. The federal government subsidizes the interest while you are actively enrolled.

Unsubsidized Loans

Unsubsidized Loans are not awarded based on financial need. Interest is charged from the time the loan is disbursed until it is paid in full. As the interest accumulates, it will be capitalized, meaning the interest will be added to the principal amount of the loan, and additional interest will then be based upon the higher amount.

2026-2027 Changes to Federal Direct Loans

On July 4, 2025, the One Big Beautiful Bill Act (OBBBA) was signed into law. Review the information below to learn about how this law impacts federal financial aid, including direct loans. While many of these changes are still being finalized, they are scheduled to take effect on July 1, 2026.

The law changes how loan amounts are calculated for students who are not enrolled full-time.

Beginning with enrollment periods on or after July 1, 2026, the following applies.

- If you are enrolled less than full-time, your federal loan eligibility is reduced (prorated) based on the number of credits you are taking.

- This means you may receive less loan funding than you have in previous years.

Typically, to qualify as a full-time student, you must be enrolled in 12 or more credit hours per semester. In certain cases, this may vary; contact Financial Aid for details.

Many students use federal loans to help cover tuition and fees, housing and rent, food and transportation, and other living expenses. If you are not enrolled full-time, you may no longer receive enough loan funding to cover these costs.

Plan your budget carefully and well in advance to avoid unexpected out-of-pocket expenses, and make informed schedule adjustments as even a small change could create a financial gap.

If you drop or withdraw from a course, the impact is immediate.

- Your loan eligibility is recalculated immediately.

- If your Fall loan has already been disbursed and you reduce your credits, your Winter loan may be reduced.

- This could leave you with a balance owed in a future term.

Before making any schedule changes, speak with your Mid Mentor and Mid's Financial Aid team to ensure you are making an informed decision. A quick conversation now could prevent future challenges and financial issues.

To avoid surprises, stay informed.

- Review your bill every time you register, drop, or withdraw from a course.

- Make sure you understand how many credits are required for full-time status.

- Typically, to qualify as a full-time student, you must be enrolled in 12 or more credit hours per semester. In certain cases, this may vary; contact Financial Aid for details.

- Meet with Financial Aid to review your funding and discuss other options if needed.

- Be realistic about your workload and plan carefully before adjusting your schedule.

We know these changes may feel overwhelming, but we've got your back! Our goal is to help you make informed decisions so you can stay focused on your academic success without unexpected financial stress.

If you have questions or would like to review your specific situation, contact Mid's Financial Aid team by emailing finaid@midmich.edu.

Federal Direct Loan Details

- Be registered in six credits or more at the time of disbursement.

- File the FAFSA.

- Be enrolled in a certificate or degree program (not as a guest student).

- Be meeting Satisfactory Academic Progress.

Before making a request, review the borrowing limits below to understand the maximum amount that could be approved. Depending on your previous borrowing history, you may not be eligible for the full amount, as Federal Direct Loans have annual and lifetime limits. Mid's Financial Aid team will review and adjust your request if needed.

With the updated loan process, you’ll need to know your enrollment plans for both Fall and Winter when submitting your loan request. You can still apply online at midmich.edu/loanrequest. If anything changes after you submit your request, contact us right away at findaid@midmich.edu so we can update your information.

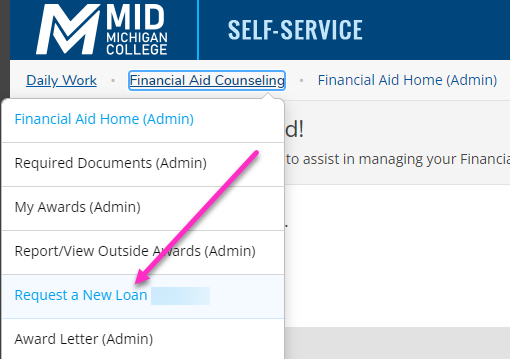

STEP 1 | Login to Self-Service and select Financial Aid.

STEP 2 | Select the Financial Aid menu at the top and click Request a New Loan.

STEP 3 | Complete the form as instructed on the screen and submit.

First Year Undergraduate 0 - 24 earned credits

- Dependent Student $5,500

- Independent Student* $9,500

Second Year Undergraduate with 25+ earned credits

- Dependent Student $6,500

- Independent Student* $10,500

*Also dependent undergraduate students whose parents are unable to obtain a PLUS loan due to not meeting credit requirements.

These examples are for sophomores, generally defined as students who have completed 30 or more credit hours.

Independent Students

You're an independent student if a contributor was not required on your FAFSA.

- Full-Time, during both the Fall and Winter Semesters, typically defined as being enrolled in 12 or more credit hours.

- Loan Maximum $9,500

- $4,750 per semester

- Loan Maximum $9,500

- Part-Time, during both the Fall and Winter Semesters, typically defined as being enrolled in less than 12 credit hours.

- Loan Maximum $4,750

- $2,375 per semester

- Loan Maximum $4,750

Dependent Students

You're a dependent student if a contributor was included on your FAFSA.

- Full-Time, during both the Fall and Winter Semesters, typically defined as being enrolled in 12 or more credit hours.

- Loan Maximum $6,500

- $3,250 per semester

- Loan Maximum $6,500

- Part-Time, during both the Fall and Winter Semesters, typically defined as being enrolled in less than 12 credit hours.

- Loan Maximum $3,250

- $1,625 per semester

- Loan Maximum $3,250

6.39% Fixed*

*Subsidized and unsubsidized loans first disbursed on or after July 1, 2025 and before July 1, 2026.

1.057% Origination Fee*

- This fee is taken before loan funds are disbursed to the school. The amount posted to your bill will be less than the requested amount as these fees have been deducted.

- The borrower is still responsible for the full amount borrowed.

*Loan fee effective on all loans disbursed on or after October 1, 2020.

Visit the Federal Student Aid website for the most current rates.

The following must be completed before a loan can be disbursed.

- Loan request submitted and confirmation of acceptance received.

- Completed MPN (master promissory note)*

- Completed Entrance Counseling*

- Final High School Transcript submitted to our office (must have the graduation date on it)

*You may have completed these steps in previous years. Log in to Self-Service and review your Financial Aid checklist items. If items are listed then you need to complete them.

Disbursement Schedule

One week before the bill due date all steps must be completed. Any incomplete loans will be canceled as of this date.

Before aid can be disbursed, we must verify your participation. After participation is verified, aid is disbursed only to those students who meet financial aid eligibility and have fulfilled all requirements.

Approximately 6-8 weeks after the start of the semester loans will be posted to student accounts.

- Loans are generally split into two equal disbursements over fall and winter semesters.*

- You must be enrolled in a minimum of 6 credits at the time of disbursement.

- If this creates a credit on your account and you are entitled to a refund, that will be available after disbursement.

*Exceptions | Students graduating after the fall semester or starting in the winter semester. A one-semester loan will be made in two disbursements during the semester.

Exit Counseling

If you previously received a subsidized or unsubsidized loan and are no longer enrolled at least half-time, which includes withdrawing or graduating from Mid Michigan College, you are required to complete Exit Counseling. You will receive an email in your Mid Mich Email account regarding this requirement, including the next steps, if you are required to complete Exit Counseling. If you plan to enroll at another institution, you still must complete Exit Counseling as there is a break in your full-time enrollment.

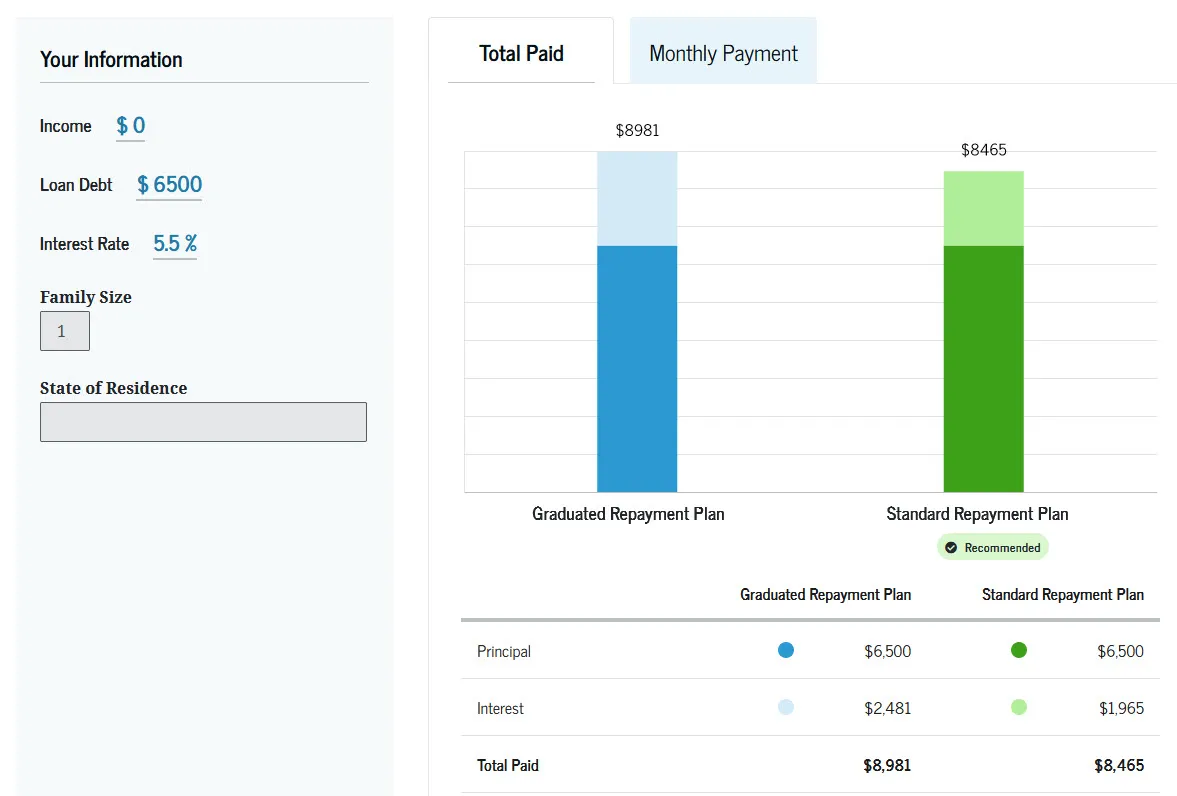

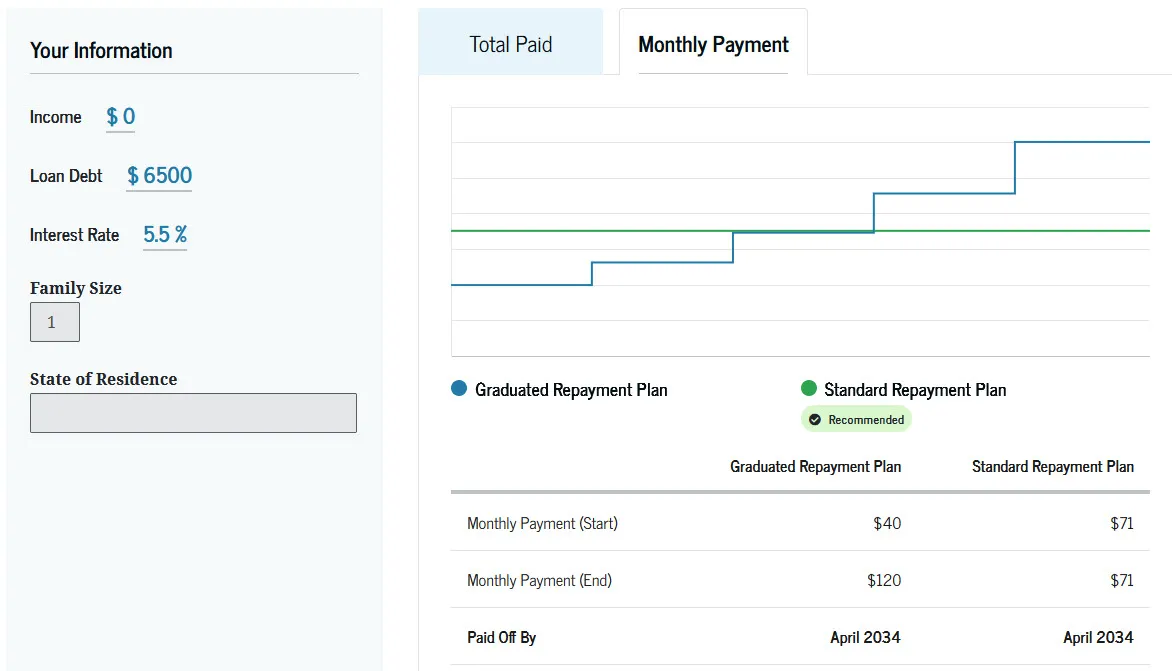

Loan Simulator

- See Your Federal Student Loan Repayment Options with the Loan Simulator.

- The Loan Simulator helps you calculate student loan payments and choose a repayment option that works best for you.

Student Loan Forgiveness

Remember, if you have missed a payment or are having trouble making payments, immediately contact your loan servicer to discuss potential options.

Student Loan Repayment via Inceptia

You’re not alone when it comes to student loans. Mid Michigan College has partnered with Inceptia, a division of the National Student Loan Program (NSLP), to provide you with FREE assistance with your Federal student loan obligations to ensure successful loan repayment.

Inceptia’s friendly customer representatives may reach out to you during your grace period to answer questions you have about your loan obligation and/or repayment options. They may also contact you if your loan(s) become delinquent. Inceptia is not a collection agency. We’ve partnered with them to help you explore a variety of possibilities such as alternative repayment plans, deferment, consolidation, discharge, forgiveness, and forbearance options. Inceptia will stay in touch with you via phone calls, letters, and/or emails to help you find answers to your questions and solutions to your issues.

For additional resources, including information on repayment options, visit Inceptia’s Federal Student Loan Overview website.

I no longer wish to borrow my loan how do I cancel it?

Send an email to finaid@midmich.edu and include the information below. This must be done within 14 days of the disbursement posting to your account. We email your Mid Mich Email account notifying you of your 14-day window. If it is past 14 days, contact Mid's Financial Aid team to see what options may be available.

- Your Full Name

- Student ID number

- Loan Type(s) (i.e. subsidized, unsubsidized)

- Amount you would like to cancel

If you cancel your loan(s) you may be left with an outstanding balance. Arrangements will need to be made immediately to pay this balance.

A cohort default rate is the percentage of a school’s borrowers who enter repayment on certain Federal Family Education Loan (FFEL) Program or William D. Ford Federal Direct Loan (Direct Loan) Program loans during a particular federal fiscal year (FY), October 1 to September 30, and default or meet other specified conditions before the end of the second following fiscal year. Refer to the Cohort Default Rate Guide for a more in-depth description of cohort default rates and how the rates are calculated.

Mid Michigan College’s current Cohort Default Rate is 0%. Learn more about how to avoid defaulting on a loan.

Federal Direct Parent PLUS Loan

Federal Direct Parent PLUS loans are available to parents of dependent undergraduate students who file a FAFSA and can be used to cover a student’s college expenses. The parent is the borrower and the loan cannot be transferred to the student.

- File the FAFSA and complete verification if selected.

- Complete the Parent PLUS Loan Application

- Complete a Master Promissory Note (MPN)

The parent must log in to studentaid.gov using their FSA ID, not their student’s FSA ID. Failing to do this will result in the application and promissory note needing to be completed again.

8.94% Fixed*

*Loans first disbursed on or after July 1, 2025, and before July 1, 2026.

4.228% Origination Fee*

- This fee is taken before loan funds are disbursed to the school. The amount posted to your bill will be less than the requested amount as these fees have been deducted.

- The borrower is still responsible for the full amount borrowed.

*Loan fee effective on all loans disbursed on or after October 1, 2020.

Visit the Federal Student Aid website for the most current rates.

Before aid can be disbursed, we must verify your participation. After participation is verified, aid is disbursed only to those students who meet financial aid eligibility and have fulfilled all requirements.

Approximately 6-8 weeks after the start of the semester loans will be posted to student accounts.

- Loans are generally split into two equal disbursements over fall and winter semesters.*

- Your student must be enrolled in a minimum of 6 credits at the time of disbursement.

- If this creates a credit on your student's account and you are entitled to a refund, that will be available after disbursement.

*Exceptions | Students graduating after the fall semester or starting in the winter semester. A one-semester loan will be made in two disbursements during the semester.

Private/Alternative Loans

Private loans, also known as alternative loans, are offered by private lenders to students as another option to cover educational expenses that may not have been covered by other financial aid. If you are eligible for Federal Direct Loans those should be used before applying for a private loan. Federal student loans are typically less expensive and offer better interest rates and repayment options.

You can apply for a federal loan through Self-Service.

You may need a co-signer as these loans are based on credit history and income.

Items to consider before applying

- Compare interest rates

- Fixed vs variable interest rate

- Repayment options

Loan Application Process

- Apply through Elmselect. There is an Apply Now button associated with each lender. You may also apply directly from a lender’s website.

- If the loan is approved, the lender sends the college an electronic certification request once the lender has received all required information from the borrower and/or co-signer.

- Once received, the loan is applied to the student’s account as pending until funds are electronically transferred from the lender to the college.

- Funds are disbursed to student accounts following our disbursement policies.

Self Certification Form - Coming Soon!

We are providing this to you but you should be supplied with one to complete during your application process with the lender.

In response to the following list, Mid Michigan College has no preferred lender arrangements for private student loans.

- Preferred Lender List and Disclosures

- Code of Conduct if Preferred Lender Arrangement

- Private Education Loan Disclosures if school provides information about a private education loan from a lender to a prospective borrower

- Private Education Loan Disclosures if preferred lender arrangement exists

Loan Code of Conduct Policy

Financial Aid at Mid Michigan College is committed to removing financial barriers for those who wish to pursue postsecondary learning, making every effort to assist students in their college fiscal planning. Mid Michigan College does not require the use of a particular lender or in any way limit the choice of lenders. Furthermore, Mid Michigan College will process loan applications through any lender a student or parent chooses. Review Mid's complete Loan Code of Conduct Policy.

Ombudsman for Students

The U.S. Department of Education provides an Office of the Ombudsman to help resolve loan disputes and problems. The following options are available for contacting the office.

- Call toll free at (877) 557-2575

- Write to

- Office of the Ombudsman, Student Financial Assistance, U.S. Department of Education

- Room 3012, ROB #3

- 7th and D Streets, SW

- Washington, DC 20202-5144

Significant effort has been made to ensure this content meets accessibility guidelines. If you encounter a barrier you can report the barrier at midmich.edu/reportaccessibilitybarrier or contact Strategic Communications at (989) 386-6622 x579 or stratcomm@midmich.edu.